By: Donald L Swanson

Chapter 12 of the Bankruptcy Code exists for the protection of family farms.

However, Chapter 12 has, from the beginning, imposed a debt limit for eligibility [Fn. 1]. This debt limit needs to be eliminated. Here’s why.

Family Farms—Then and Now

Back in 1986, at enactment of Chapter 12, the vast majority of farms were owned and operated by members of a single or extended family.

The same is still true today. The differences are that today’s farms:

- are owned and operated by later generations of the same families who owned and operated farms back in the 1980s—these are the families who managed to survive as farmers to the present day;

- are much, much larger and operated by fewer people than in the 1980s—farming has progressed from intense labor with small equipment in 1980s to limited labor with huge equipment, computers and GPS precision today; and

- have much, much larger amounts of debt than in the 1980s—today’s capital requirements for farm land, equipment and inputs dwarf those of the 1980s.

Corporate Farms & Chapter 12 Eligibility—Then and Now

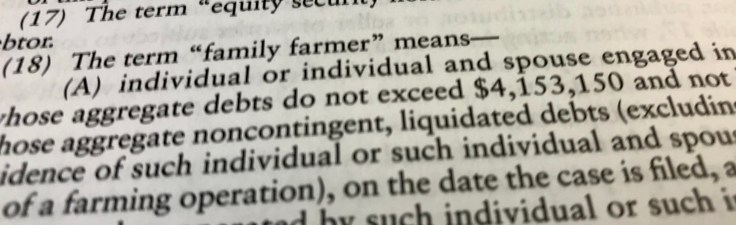

Back in the 1980s, corporate farms existed—i.e., farms owned by investors who were unrelated to each other. But those farms failed to qualify for Chapter 12 relief because of “family” requirements for eligibility. Such “family” requirements include these [see § 101(18)]:

(i) “individual or individual and spouse” must be “engaged in a farming operation,”

(ii) More than 50% ownership must be “by one family” or “the relatives of the members of such family,” and

(iii) “such family or such relatives” must “conduct the farming operation.”

Corporate farms exist today, as well, but these farms fail to meet the “family” eligibility requirements for Chapter 12—just like the 1980s.

It is these “family” requirements that are the essence of Chapter 12 eligibility.

Reasons for Debt Limits on Eligibility?

It’s difficult to see or understand the reasons for a debt limit on Chapter 12 eligibility.

Keeping family farmers, with large amounts of debt, out of Chapter 12 may have made sense back in the 1980s when nearly all family farms were small—and those with more than $1.5 million of debt were a rarity.

But in today’s world, every family farm, where the family makes its primary living from farming, is large. Multi-millions of dollars of debt are common for such farms—even the smaller ones.

The debt limit confuses large family farms with corporate farming.

Debt Limit Makes No Sense Today

The debt limit for Chapter 12 eligibility no longer makes sense. Here’s why:

The goal of Chapter 12 is to provide effective bankruptcy relief for family farmers; and

A family farm is identified by its “family” character—not by the amount of its debt.

Back in 1986, when Chapter 12 was adopted, there were lots of small farms operated by career farmers. That reality translated into lots of people living in rural America. But those days are gone. And the small, career farms are gone as well.

Today, small farms are owned and operated by part-time or hobby farmers—people with other sources of income. And these people are unlikely to qualify for Chapter 12, because of such eligibility requirements as these:

(i) 50% of gross income must come from farming;

(ii) 50% of debts must arise from farming; and

(iii) farm assets must comprise more than 80% of all assets.

So . . . if small, non-career farms don’t qualify for Chapter 12, who is it we are trying to help? The answer is obvious: it’s the career farms that qualify as family farms, regardless of size. And these farms—all of them—can have large, even staggering, amounts of debt.

Inequities of the Debt Limit

Consider this family farm:

Four brothers have been running a farming operation, using a single corporation. All four are career farmers, and each owns 25% of the corporation. The corporation has $12 million of debt, which each brother has personally guaranteed. The corporation is in financial trouble, is in default on its primary debts, and is insolvent.

–Hypothetical # 1

One brother, over the years, has acquired land and machinery in his own name. He wants to leave the family farming operation and farm his own land. And he wants to utilize Chapter 12 to deal with the debt he has guaranteed. But he can’t because the amount of his guaranteed debt makes him ineligible.

–What is fair or equitable or defensible about that?

–Hypothetical # 2

The brothers want to reorganize their farming operation under Chapter 12. But they can’t because it has $12 million of debt. Never mind that the total debt averages $3 million per brother (which is within the current eligibility limit)—but the eligibility statute is too blunt to allow for such distinctions.

–What is fair or equitable or defensible about that?

The four brothers, in the two hypotheticals above, are precisely the family farmers that Chapter 12 is designed to help. But it is precisely these people who can’t use it because of the debt limit. There is something wrong with that.

A Policy Choice for Congress

–A Sentence to Liquidation

Chapter 12 exists because Chapter 11 did not work for farmers in the 1980s. Back then, a Chapter 11 filing was, in effect, a sentence to liquidation — and this has not changed in the intervening decades.

So, using the debt limit, today, to keep a family farm out of Chapter 12 and requiring Chapter 11, instead, is a sentence to liquidation of the family farm.

Is this really what Congress wants? Does Congress truly intend that the four brothers, in the hypotheticals above, should be required to liquidate, instead of using Chapter 12 to reorganize—solely because of their debt amount?

–A Brain and Talent Drain

If the four brothers, in the hypotheticals above, are required to liquidate in Chapter 11, rather than reorganize in Chapter 12, what’s the benefit of that? The answer is this: there is none.

On the contrary, there is great value for rural communities in retaining entrepreneurs and family farms.

An alternative is to have the same land managed by someone living in Lincoln or Omaha or Des Moines or Iowa City, who employs hired hands to do the labor. That alternative would accomplish a significant drain of human resources out of our rural communities.

–Is that what Congress wants to accomplish by a debt limit on Chapter 12?

The Debt Limit is an Arbitrary Number

Here’s how we got to today’s debt limit amount for Chapter 12 eligibility:

–Debt limit of $1,500,000 was established in 1986 at enactment of Chapter 12;

–Thereafter, the $1.5 million number adjusted periodically to reflect changes in the Consumer Price Index [Fn. 2];

–Debt limit of $3,237,000 was established in 2005 at enactment of the Bankruptcy Abuse Prevention and Consumer Protection Act—this number appears to be the $1.5 million 1986 amount, adjusted with the Consumer Price Index; and

–Today’s debt limit is $4,153,150 — this is nothing more than the 2005 amount, as adjusted with the Consumer Price Index.

–Meaningless Number and Concept

So . . . we are living today with an eligibility number established more than three decades ago, adjusted only for inflation. This is a meaningless number. Farming has changed drastically in the meantime—far beyond mere adjustments for inflation.

But more fundamentally, the very concept of a debt limit for eligibility is arbitrary.

Who’s to say that a family farmer with $4.09 million of aggregate debt is deserving of Chapter 12 relief, while someone with $4.16 is not? Or someone with $10.5 million is not? Or someone with $15 million is not?

If a farm is truly a family enterprise, Chapter 12 relief should be available. After all, if Congress went to all the trouble to create a bankruptcy remedy for family farmers, why seek to prevent its use by an arbitrary and meaningless number?

Conclusion

Chapter 12 exists to help family farmers. And we should no longer exclude family farmers from Chapter 12 by an arbitrary and meaningless debt limit.

Footnote 1: Chapter 12 eligibility standards, for a family farm, are identified in 11 U.S.C. § 101(18)-(21).

Footnote 2: Adjustment for inflation, using the Consumer Price Index, is required by 11 U.S.C. § 104.

** If you find this article of value, please feel free to share. If you’d like to discuss, let me know.

Leave a comment