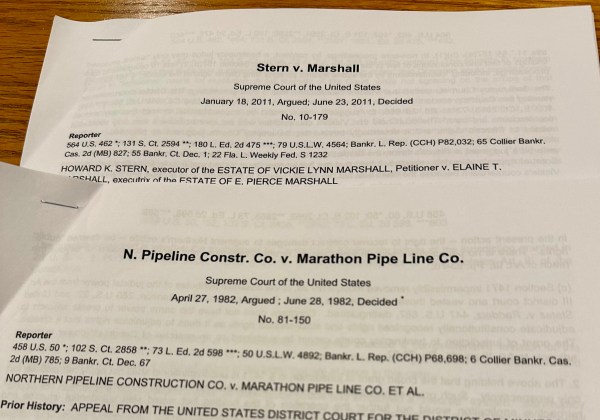

Northern Pipeline & Stern Opinions By: Donald L Swanson The U.S. Supreme Court has never liked like the Bankruptcy Code and has worked diligently, over the decades, to limit the authority of bankruptcy courts and bankruptcy judges. Two examples are U.S. Supreme Court opinions that have anniversaries this month—in June of 2026: 44 years ago (on... Continue Reading →

Northern Pipeline v. Marathon And Stern v. Marshall: Bankruptcy Law Run Amok (Part 3)