For starters, see my “Disclaimer” below.

“The Torah is the Hebrew Bible,” consisting of the books of Genesis, Exodus, Leviticus, Numbers, Joshua, Psalms, Book of Ruth, etc.; and the Talmud “is the compilation of the historical rabbis ‘discussing’ or ‘debating’ what the Torah means.” [Fn. 1] The Mishnah is “an edited record” of “material known as oral Torah.” [Fn. 2]

The Torah, the Talmud and the Mishnah have much to say about bankruptcy-type issues. Their provisions protect debtors from oppressive conduct, authorize repayment plans, and authorize exemptions, discharge and a fresh start [Fn. 3].

Such provisions are of ancient origin but are still with us today as central features in our own Bankruptcy Code. The following is an attempt to explain.

PART I — Protecting the Debtor

“Everyone has to pay their debts but not everyone can, so the question arises what to do when a borrower is insolvent.” One solution is bankruptcy.

Today’s Bankruptcy Code provides for the welfare of both the debtor and creditors. It authorizes both, (i) payment plans over time in chapters 11, 12 and 13, and (ii) immediate discharge and surrender of non-exempt assets under Chapter 7.

Both procedures “have precedents in Judaism.” But in Jewish tradition the “foremost” consideration is “the well-being of the debtor.”

–Torah Commandments Protecting Debtor

The following Torah commandments protect a debtor “from excessively harsh collection actions” and provide for a fresh start [Fn. 4]:

1. “When you lend money to My people, to the poor man among you, do not press him for repayment. [Also] do not take interest from him” (Exodus 22:24) [i.e., do not harass a debtor];

2. “If you take your neighbor’s garment as security [for a loan], you must return it to him before sunset. This alone is his covering, the garment for his skin. With what shall he sleep? Therefore, if he cries out to Me, I will listen, for I am compassionate” (Exodus 22:25-26, see also, Deuteronomy 24:12-13) [i.e., a pledge of collateral should not create hardship for or pressure the debtor];

3. “When you make any kind of loan to your neighbor, do not go into his house to take something as security. You must stand outside, and the man who has the debt to you shall bring the security outside to you.” (Deuteronomy 24:10-11) [i.e., treat a debtor with dignity];

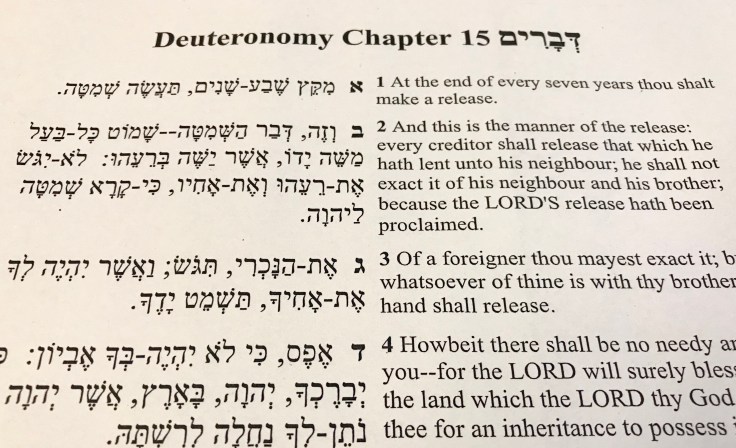

4. At the end of every seven years, you shall celebrate the remission year. The idea of the remission year is that every creditor shall remit any debt owed by his neighbor and brother when God’s remission year comes around. (Deuteronomy 15:1-2) [i.e., a discharge of debts is authorized to create a fresh start].

Such provisions are reflected, still today, in our Bankruptcy Code and related laws.

PART II – Bankruptcy Plans and Exemptions

–Bankruptcy Plans

A “payments arrangement for an insolvent debtor” is a possibility in bankruptcy. One historical source of such an arrangement is this: “the laws of Temple donations.”

Here’s what the Torah provides:

“If [a person] is too poor to pay the endowment, he shall present himself before the priest, so that the priest can determine the endowment valuation. The priest shall then make this determination on the basis of how much the person making the vow can afford” (Leviticus 27:8).

The Talmud indicates that laws concerning debtors, in general, are more lenient than those for someone who made a donation commitment. So, any leniency to a poor person involving a Temple donation would also apply “to any poor person” (Babylonian Talmud Bava Metzia 114a).

–Bankruptcy Exemptions

The Mishnah provides exemptions from creditors for food, wearing apparel, household goods and furnishings, and tools of trade:

“Although assessment debtors may have their property seized, they must be left enough food for three meals, and clothing for twelve months, a bed and bedclothes and tefillin” (Mishna Archin 6:3); and

“If he is a workman we leave him his work tools, from each kind” (id.).

The Torah also provides a tool-of-trade exemption:

“Do not take an upper or lower millstone as security for a loan, since that is like taking a life as security” (Deuteronomy 24:6) [a millstone is a tool for earning a livelihood].

Such provisions teach that, (i) “taking a person’s livelihood is like taking his life,” and (ii) “if a person can’t earn a living, he will be unable to pay back the debt.” The emphasis is on “the human aspect of the law” and “rejects a punitive approach to debt repayment” in favor of “a constructive and rehabilitative approach.”

Rejection of a punitive approach “is a consistent theme in Jewish literature.” Torah law provides:

When a creditor demands payment, the debtor retains essential assets, while the rest is given to the creditor; but

“We do not arrest him, nor ask him to bring proof that he has no other assets” (Maimonides Code, Laws of Loans 2:1).

[Editorial Note: We did not outlaw debtors’ prison in the U.S. until the 1830s.]

The essence of such provisions is to allow an insolvent debtor to keep basic-and-essential assets and to be free from counterproductive or vindictive collection actions, while arranging a repayment schedule for paying debts “to the best of his ability.”

Such provisions are with us to this day in state and federal laws.

PART III – Discharge of Debts and a Fresh Start

The Torah also provides for a discharge of debts:

“At the end of every seven years, you shall celebrate the remission year. . . . if you have any claim against your brother for a debt, you must relinquish it.” (Deuteronomy 15:1 & 3).

This provides a “fresh start” to debtors: “a new lease on life that will give them the ability and the incentive to become productive citizens.”

Rules arose, over time, to circumvent the release of debts, because excessive leniency ultimately works to a debtor’s disadvantage—e.g., credit becomes unavailable. So, the lesson is this: while allowing a fresh start is a worthy ideal, “sometimes the economic and social conditions make it counterproductive.”

Moreover, Judaism considers paying debts a positive obligation – a mitzvah (Babylonian Talmud, Ketubos 86a). So, a debt must be incurred “with good faith and with reason to believe” that it will be repaid, and the debtor must “make every effort to obtain the means to fulfill his obligation.”

Unexpected setbacks can make repayment impossible. In such circumstances, the Torah points to the “ideal of . . . a fresh start.” This ideal is a central feature of today’s bankruptcy laws.

CONCLUSION

The Torah, the Talmud and the Mishnah are of ancient origin. Yet, the bankruptcy-type rules they contain are still in effect today – and many of those rules still serve as a centerpiece of today’s Bankruptcy Code.

This is remarkable, indeed!

—————-

Footnote 1: These quotes are from, “What is the difference between the Talmud and the Torah?”

Footnote 2: This definition is from, “What is the Mishnah?”

Footnote 3: Information in this article that touch on religion and quotations are (unless otherwise noted) from three publications by Rabbi Dr. Asher Meir, collectively titled, “The Morality of Bankruptcy,” and consisting of Part I, Part II and Part III.

Footnote 4: All Torah quotations are from “The Living Torah” translation.

DISCLAIMER: In this blog, I try to avoid topics of religion and partisan politics. But the subject above is fascinating and pertinent, so I decided to go with it anyway. It’s, mostly, a summary of Rabbi Meir’s three-part article linked in Footnote 3. My article is flawed [I know this because a friend with expertise on the subject politely declined when asked for feedback on an early draft of this article]. So . . . please read Rabbi Meir’s three-part article in its entirety.

** If you find this article of value, please feel free to share. If you’d like to discuss, let me know.

Hi thanks for sharring this

LikeLiked by 1 person