By: Donald L Swanson

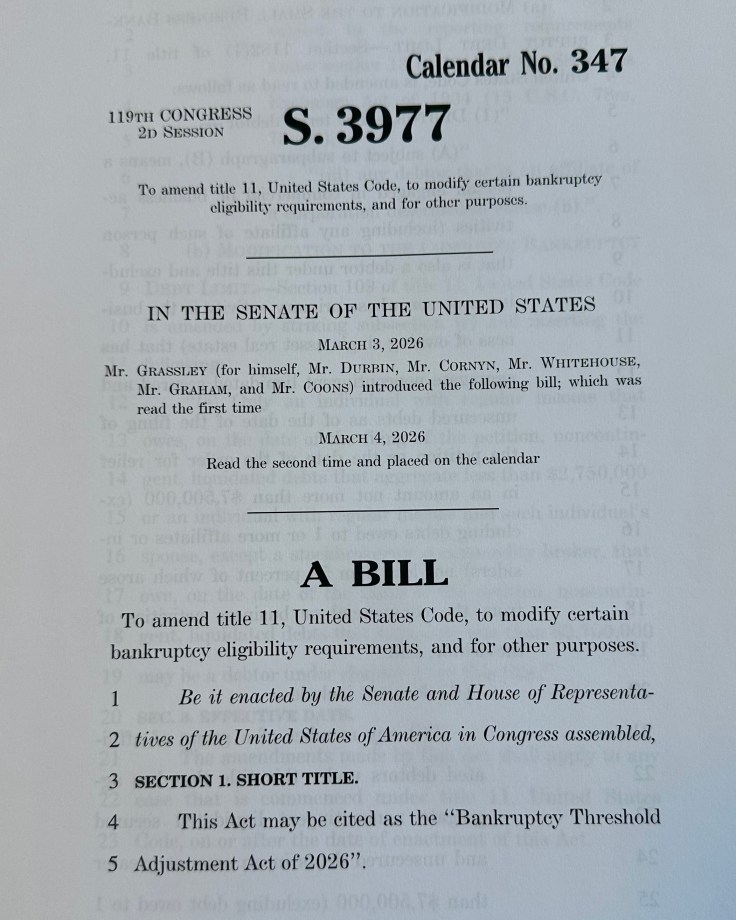

On March 3, 2026, six Senators (three from each party) introduced S. 3977, titled the “Bankruptcy Threshold Adjustment Act of 2026.”

The six senators are Chuck Grassley (R-IA), Richard Durbin (D-IL), John Conyn (R-TX), Sheldon Whitehouse (D-RI), Lindsey Graham (R-SC), and Christopher Coons (D-DE).

Here is a link to the Congress.Gov webpage for S. 3977.

The essential features of S. 3977 are these:

- it sets the debt limit for Subchapter V eligibility at $7,500,000;

- it sets the debt limit for Chapter 13 eligibility at $2,750,000;

- it provides that the new debt limits “shall apply to any case that is commenced . . . on or after the date of enactment of this Act”; and

- it does not contain any sunset provision.

A Fighting Chance

I believe that S. 3977 has a fighting chance of getting enacted relatively soon. What follows are some reasons why.

Bankruptcy Law is Mostly Nonpartisan & Apolitical

In most circumstances, bankruptcy law is nonpartisan and apolitical. The effect is that partisanship—even hyper-partisanship—won’t stand in the way of a bankruptcy law enactment that’s needed.

The reason is because nobody likes bankruptcy. And its also because partisans have a hard time getting worked up over bankruptcy issues like cash collateral and adequate protection and absolute priority rule.

Illustrating the nonpartisan and apolitical reality for bankruptcy law is the history of Subchapter V itself:

- Subchapter V was enacted as part of the Small Business Reorganization Act in August of 2019, which was signed into law by a President from one political party; and

- then, Congress increased the amount of the Subchapter V debt limit from $2,750,000 to $7,500,000 in March of 2020, which was signed into law by a different President from a different political party.

Both such times (August 2019 and March 2020) can be characterized as a hyper-partisan times with similarities to today’s hyper-partisanship. Yet, such hyper-partisan realities did not impede or prevent the Subchapter V enactment and amendment that occurred.

Moreover, the nonpartisan and apolitical nature of bankruptcy law is apparent from unanimous and nearly-unanimous bankruptcy opinions from the U.S. Supreme Court. Recent examples are City of Chicago v. Fulton (2021) and Bartenwerfer v. Buckley (2022).

Bankruptcy Enactments & Expected Downturns

Most bankruptcy law enactments have occurred in response to financial stress. For example:

- the first federal bankruptcy Act (of 1800) was enacted to get prominent people from the Revolution effort (e.g., Robert Morris) out of debtor’s prison:

- Chapter 12 was enacted as a response to the 1980s Farm Crisis; and

- the increase of Subchapter V’s debt limit in March of 2020 to $7,500,000 was the direct result of the Covid 19 Pandemic and the expectation, back then, of a resulting economic downturn.

In today’s political landscape, a lot of discussion occurs about the future of our economy and the possibility of a downturn that may happen or is already in progress. In such a context, the political calculation is this:

- in an economic downturn, every constituent of every politician is a potential debtor; and

- no politician wants to be seen as standing in the way of protecting constituents in an economic downturn.

Political Realities & Effects

Everyone knows that strong interests in these United States are against anything involving bankruptcy—as a matter of reflex. The reflex goes like this:

- “It’s a bankruptcy bill? I’m against it! What does it say?”

Opponents of a bankruptcy bill—especially a bill with strong public support—have some tools they commonly use. One such tool is a sunset provision—i.e., the new law will go away in a couple years when economic downturn concerns are, hopefully, behind us. The sunset tool has been used effectively in Subchapter V to do these two things.

- The first effect is to prevent the $7,500,000 debt limit from becoming permanent—which has been successful thus far. We’ve been on the lower debt limit for Subchapter V eligibility for nearly two years—which lower limit has prevented many businesses from obtaining effective bankruptcy relief.

- A second effect is to prevent a consumer price index increase on the $7,500,000 debt limit. Had the $7,500,000 debt limit been permanent from the beginning, with the consumer price index adjustments applying, that limit would have increased by now to over $9,000,000. But, instead, we are still talking, in S. 3977, about the $7,500,000 number.

By contrast, there is no such thing as debtor representation in the halls of Congress. There is, for example, no such thing as a “National Association of Bankruptcy Debtors.” Nor is there any aspirational organization like a “Future Debtors of America.”

The effect is that bankruptcy amendments are hard to accomplish, except in the context of an existing or expected economic downturn.

Voldemort of Bankruptcy Legislation

Back in June of 2024, a bankruptcy amendment to extend the $7,500,000 debt limit was before Congress on a unanimous vote type of procedure in both houses of Congress.

At that time, everyone (we were told) in both houses of Congress was ready to vote “Aye” on that extension—except for one Senator. That means 435 members of the House and 99 members of the Senate were prepared to vote “Aye” on extending the $7,500,000 debt limit for Subchapter V.

But one Senator defected and would not go along. The identity of that Senator is well known. But for reasons unknown (at least to me), that Senator’s name is rarely mentioned in public. So, I’ve dubbed that Senator the “Voldemort” of bankruptcy legislation: the One-Who-Must-Not-Be-Named.

Further, that Senator was obviously (i) carrying water for the anti-bankruptcy interests (who also, apparently, must not be named), and (ii) enabling other Congress members to achieve the desired result of no debt limit extension while appearing to be in favor of it.

Perhaps, the existing economic and political context will overcome Voldemort’s contrarian position.

Conclusion

A new bill for resurrecting the $7,500,000 debt limit for Subchapter V eligibility (S. 3977) is now before Congress.

And it appears to have a fighting chance of passage.

We can always hope!

** If you find this article of value, please feel free to share. If you’d like to discuss, let me know.

Leave a comment